Big Problem, Small Data

Insurance was and is centered on data. In fact, one insurer COO recently told me that what incumbents have over insurance startups is data and customers. Note, though, he didn’t mention actionable data, and actionable data need not be the outcome of Big Data.

I’m a fan of Big Data as much as the next guy.

When I joined CNA, one of my first projects was to analyze quoting data – basically rows and rows of quote numbers, account names, locations, premiums, producer codes, and specific coverage values. I may have learned that one day of the week was busier than the other, that the average premium was so and so, and that the majority of agents picked the same limits for deductible and GL – but who could really tell if that was the case of causation or correlation, as popular limits were, often times, the default limits. This effort produced zero actions. I later moved on to equipping CNA’s field sales specialists with a monthly summary of their accounts, e.g. how many agents closed how much business, in which area, and what line of business etc. This was a largely manual effort that may or may not have produced a more intelligent conversation between sales and producers. Or so, I hoped.

But hope is not a strategy and what doesn’t get analyzed, doesn’t get improved. And with more and more insurers turning to digital – we’re witnessing improvements in distribution, claims and underwriting. The latter – being employee-facing – generates a lot less buzz as companies keep their strategies and offerings at a bird’s-eye view; touting data science and continuous real-time underwriting, while leaving a lot of the details behind.

But the devil is in the details, so before sitting down with Marcus Daley, the technical co-founder of NYC-based NeuralMetrics, I conducted a 30-minute phone interview with one of his clients who works for one of the largest publicly traded P&C insurers and who has asked to remain anonymous (see note above about insurers keeping their cards to themselves).

“Let’s say you go to a traditional data vendor, they will give you 200 attributes, and we look at them and say ‘we only need five of them’, the rest of them is ‘nice to have’. Whereas the model with NeuralMetrics is very different. The model with NeuralMetrics is – we go to them and give them a list of 200 questions and ask ‘how many can you answer?'”

By the time this particular insurer reached NeuralMetrics , an alternative data engine that delivers classification, underwriting, know your customer, and intelligent prospecting to commercial lines insurers, it had already experienced solutions from other insurance technology companies and was looking to solve for: (1) inaccurate data entered by agents, (2) a lack of unified and comprehensive view of the business, (3) a poor user experience as agents and wholesalers were often faced with 50 to 60 underwriting questions, and, most importantly, (4) it was looking to address the zero underwriting that takes place from when a policy is underwritten and issued, to the time it’s up for renewal.

You could say with certainty, this business professional knew exactly what they wanted.

When NeuralMetrics entered the picture, it offered a web intelligence solution that identified the online presence of particular businesses and looked for evidence of adverse risks. The startup ran the entire book of business through this engine to start flagging businesses that triggered an alert based on the insurer’s risk appetite. “Tailor-made for us,” is how the client went on to describe the solution by NeuralMetrics, acknowledging the fact that every insurer has different underwriting guidelines and specific needs. Ultimately, NeuralMetrics solved for “on average, 70-80%” of the questions and automated what was once a job of 20 to 30 interns ‘over the summer.’

For Marcus, this is a technology problem and an information services problem; areas he considers his roots, as he knows more than a thing or two on providing information on businesses and their customers – having been the CTO for S&P Global Market Intelligence/CapIQ and other information services businesses. And while Marcus is new to insurance, he sees a real need to be able to get information on private or small businesses to assess risk more quickly and more accurately, and it was this understanding that led Marcus to become an integral part of the NeuralMetrics team. In fact, Coverager’s first face-to-face meeting with the team, was indeed with Marcus and a fellow colleague. “We can all get our head around risky behavior” and so the problem is very straight forward but isn’t straight forward to solve, he tells me.

And I couldn’t agree more.

My data experiment at CNA was by no means a ‘must-have,’ hence the fuzzy outcome. This particular case study with NeuralMetrics alludes to the importance of doing the basic groundwork before bringing a data partner onboard. For instance, breaking books of business to unique and homogeneous books to create a defined need. After all, small business is specific business and a data solution is only as good as the specifics it uncovers. A different way to look at this is by considering the rise in new, yet niche, small commercial players such as Next Insurance, Three or Harborway Insurance, in comparison to Insureon, Nationwide or Progressive that underdeliver in their attempt to create a single solution to meet the needs of ‘small business’ insurance customers.

One defined need can be solving the data problem associated with entrepreneurs, who find it normal to pivot as they assess growth opportunities. Yet, from an underwriting perspective, adding or removing services may impact the nature of the business; and hence the risk associated with that business. “A big problem,” as Marcus puts it. And while Big Data is an accurate term when it relates to the number of businesses and the aggregate of all the information attributes gathered, this isn’t a Big Data problem. “But the problem itself on an individual business basis – one small business – is not a Big Data problem. They don’t have that much data about them. It’s actually the opposite – a small data problem, where they may have only said a few things about themselves using specialized terms. Small businesses often only have a very rudimentary website describing the business. They may have a few places where they’ve had to file information because they’re not a public company. Their social media presence may not be that large and may be their only web presence. Although we do find that many spend quite a bit of time in social media. And so it’s a small data problem, which creates our advantage, I believe. In order to be successful with what we’re doing we take an approach that works well with small data while still allowing us to convey truth and to accurately identify those risks. We’re not necessarily applying Big Data techniques to a small data problem.”

It’s the techniques and not the technology that insurers should be focused on when trying to answer what works for them; after all, any data initiative is a journey. “It’s been a journey trying to figure out what will work and we’ve approached it from a whole host of different angles trying a lot of different tools and techniques and feel like we’ve built up a pretty good understanding of what does and doesn’t work. We kind of got caught up in that Big Data view of the world initially but then eventually figured out that, hey, this is actually a small data problem.”

Also, according to Marcus, the baseline here is not ‘perfection.’ People want to see ‘perfection with the machine doing the work, but in reality, what they have today is agents doing the work, and agents have a tendency to be 60-70% accurate, if they’re lucky, and often times it is much worse than that, and that’s not a knock on agents as it is simply a reflection of what they are told. And a lot of times these small businesses don’t know how to answer the question, you know, they’re doing their best but insurance isn’t what they do. The baseline is ‘what are you getting from the agent?”

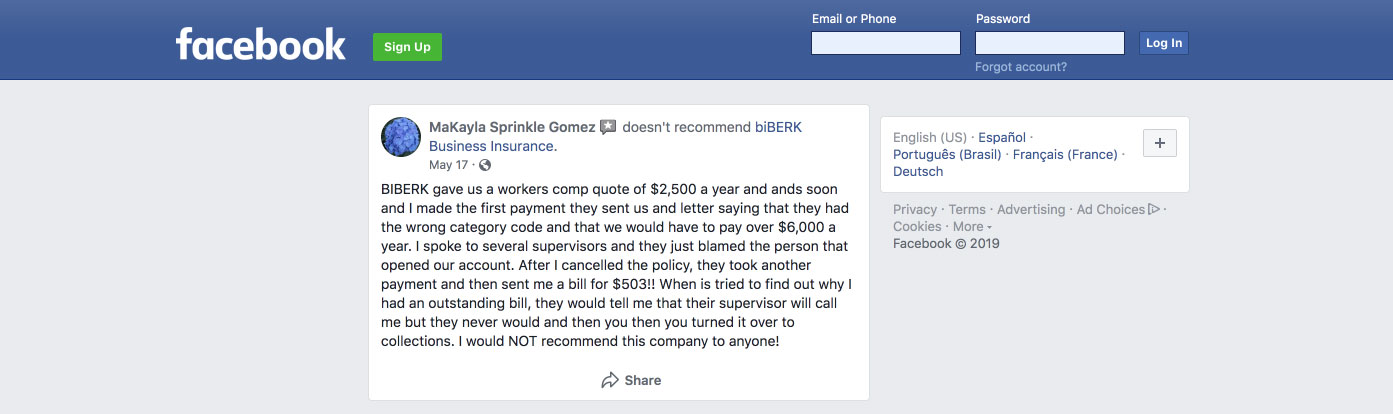

Perhaps another baseline, is what are you’re getting from the online shopper? Consider why MaKayla Sprinkle Gomez doesn’t recommend biBERK Insurance:

Marcus, who drives a Tesla that’s insured by Travelers, and has recently listened to “a really depressing book, but it’s actually a great lesson in getting fanatical about terms like Big Data” called Bad Blood, acknowledges the amount of bad data found in any data initiative and the challenges with working on bleeding edge technology – no pun intended. You will not hear him make big promises as he’s a man that focuses on perfecting the process to achieve optimal results.

I can relate.

I recently joined Orangetheory Fitness and what I enjoy the most is that every new milestone I achieve is relative to my personal best. To me – that’s the value of working with NeuralMetrics – they look to help insurers achieve their personal best relative to the data they have, yet specific to their underwriting core.