The democratization of road safety – How insurance and telematics will lead the way

In our world today, an unprecedented pandemic plagues our roads. Traffic accidents claim the lives of millions every year, with nearly 3,700 people losing their lives each day in crashes involving various modes of transportation. To put this into perspective, the average daily death toll due to COVID-19 over the last 3.5 years stands at 5,300. The need for democratizing road safety has never been more critical.

Democratization of road safety entails three crucial elements; access to superior road infrastructure, modern vehicles equipped with advanced safety features, and comprehensive information and training for drivers. While this may seem like an insurmountable challenge, the insurance industry can step up as the hero in this narrative and contribute significantly to safer roads.

Risk assessment capabilities

Leveraging their vast data, insurers possess the ability to assess risks accurately. This information can be used to identify high-risk areas and influence policy and regulation, promoting evidence-based decision-making.

Risk mitigation through education

Insurers can actively contribute to road safety by providing educational resources and raising awareness about safe driving practices. By partnering with communities, they can engage in initiatives that go beyond their traditional customer base.

Collaboration and partnerships

Insurers have the opportunity to collaborate with various stakeholders to drive road safety initiatives forward collectively. Stakeholders include government agencies, NGOs, and technology providers,

Driver monitoring technology

The implementation of telematics devices, mobile apps, and advanced sensors allows insurers to monitor and assess driver behavior accurately. This data-driven approach enables personalized feedback and interventions, ultimately improving road safety.

Shared-value insurance initiatives

Shared-value insurance initiatives create a win-win situation where the insurer, insured, and society at large benefit. These initiatives go beyond selling policies and prioritize proactive risk mitigation and prevention. Let’s explore how they benefit insurance companies:

- Community engagement: Shared-value programs actively engage with communities and individuals beyond the insurer’s typical customer base. By reaching out and addressing their needs, insurers establish a positive presence and build relationships.

-

Risk mitigation: Rather than focusing solely on policy sales, shared-value initiatives emphasize proactive risk mitigation and prevention. By addressing the root causes of accidents, insurers contribute to safer roads and reduce claims.

-

Brand reputation and trust: By offering free disaster preparedness and education programs, insurers demonstrate their commitment to corporate social responsibility. This enhances their brand reputation and builds trust among potential customers who appreciate their efforts in promoting safety and resilience.

-

Business growth potential: While the primary goal is to benefit society, shared-value initiatives indirectly support business growth. Establishing a positive brand image, fostering trust, and positioning themselves as experts in disaster preparedness can attract new customers and lead to increased policy sales.

Notable examples

Two notable examples of shared-value insurance initiatives are the OUTsurance Pointsmen Project and AXA’s “Know You Can” campaign. The former tackled traffic congestion and road safety issues caused by power outages, while the latter focused on raising awareness about climate change and encouraging sustainable behaviors.

The latter AXA – “Know You Can” campaign in the UK aimed to raise awareness about climate change and encourage individuals to take action. The campaign featured TV commercials and online videos highlighting the impact of climate change and the role individuals can play in making a difference. AXA promoted sustainable behaviors such as reducing energy consumption AND using public transportation.

The power of mobile telematics

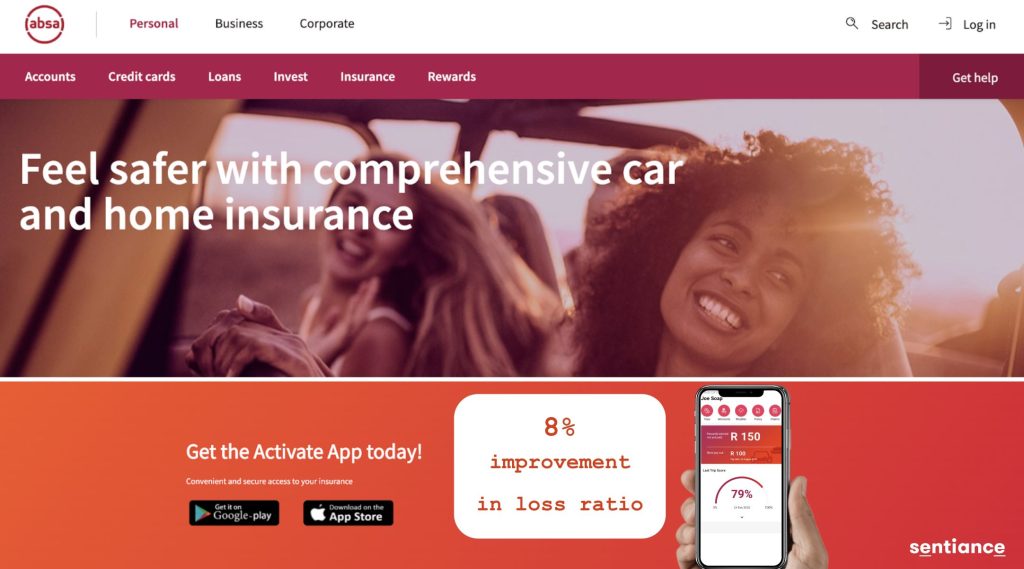

Mobile telematics technology aligns perfectly with the ethos of shared-value insurance initiatives. It has already proven its effectiveness in Usage-Based Insurance (UBI) programs, providing valuable insights into driver behavior and risk factors. Successful campaigns, such as Absa’s UBI program and RAC’s RAC Go App, have showcased significant improvements in road safety without solely relying on financial rewards.

Challenges and solutions

Despite the potential of mobile telematics, several challenges hinder its widespread adoption. Concerns about data privacy and security, slower customer adoption and engagement, and the high cost of implementing telematics technology are the primary obstacles. However, advancements in Sentiance on-device technology addresses these challenges by ensuring secure data processing and reducing the costs of technology by up to 90%.

In conclusion, the democratization of road safety requires collective efforts from various stakeholders, including the insurance industry. By embracing shared-value insurance initiatives and harnessing the power of mobile telematics, insurers can play a pivotal role in reducing accidents, saving lives, and promoting safer roads. With the right partnerships and innovative technologies, the vision of democratizing road safety can become a reality. Get in touch to explore how we can collaborate to create a safer and more secure future for all.